.jpg)

EU-UK Spotlight: Renewables, trade, and the global supply chain

Search

Search

Search

Search

On 28 April 2026, the FCA published Consultation Paper CP 26/14 – Changes to information flows for UK equity IPOs (CP 26/14), setting out proposed changes to the rules governing information flows during UK equity initial public offerings (IPOs). The consultation focuses principally on the rules introduced in 2018 under COBS 11A, which were designed to encourage the production of unconnected research and mitigate perceived conflicts of interest in connected research during IPOs. Since their introduction however, the FCA has received consistent feedback from market participants that the rules have not achieved their intended purpose and have instead introduced unnecessary market friction. Consequently, the FCA proposes changes to address these concerns which we summarise below.

In July 2018, the FCA introduced a package of rules designed to improve the quality and availability of information during the UK equity IPO process. Overall, the reforms sought to address perceived risks of bias in connected research coverage, promote the availability of unconnected research and ensure that an FCA-approved prospectus was the primary source of information for investors in an IPO process.

Specifically, the 2018 changes to the COBS rules:

Consequently, the publication of the FCA-approved prospectus or registration document mark the start of the ‘public-phase’ in the IPO process, with the subsequent publication of research reports. Issuers and their advisers could then determine whether to:

Since the changes were introduced, the FCA notes that joint briefings with connected and unconnected analysts have rarely been conducted in practice, due to commercial considerations and the increased risk of deals being inadvertently leaked in advance of an ITF announcement. In practice, this has meant that issuers have had to opt for a ‘7 day-delay’ by default, unnecessarily extending the IPO process and consequently, putting the UK at a comparative disadvantage relative to other listing venues. Additionally, the FCA understands that the changes allowing unconnected analysts equal access to information have not led to the increase in independent research reports, which have been found to be limited in detail and not widely distributed.

In CP 26/14, the FCA proposes two principal changes to the COBS 11A unconnected analyst rules:

Removal of the 7-day waiting period for connected research. The FCA proposes to amend COBS 11A.1.4FR to remove the 1-day/7-day waiting period between the publication of an approved registration document or prospectus and the publication of connected research. Firms will be able to publish the approved registration document or prospectus and any connected research simultaneously.

Removal of the equal information sharing requirements. The FCA proposes to remove COBS 11A.1.4BR to COBS 11A.1.4ER, which mandate that syndicate banks intending to publish connected IPO research share the same information with a range of unconnected analysts as they do with their own research analysts.

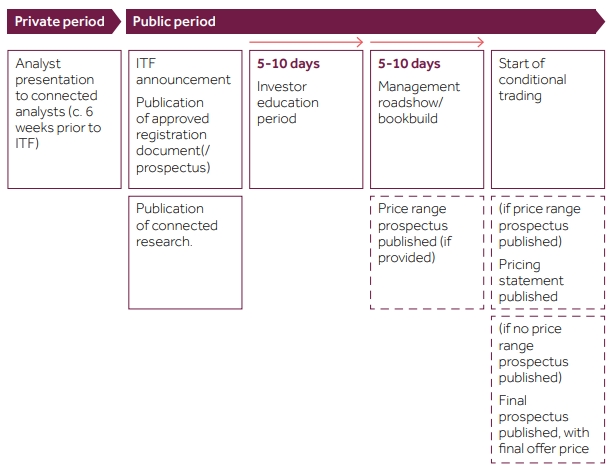

Consequently, the indicative timeline for an IPO would look as follows:

FCA CP 26/14 - Figure 2: Indicative timeline of key events during equity IPO process, following proposed changes.

The FCA emphasises that the rule changes would not prevent unconnected analysts from requesting information from issuers in order to produce research, or from attending analyst briefings. Indeed, issuers and unconnected analysts will be able to contact each other directly to discuss research coverage.

The FCA is also taking the opportunity to correct a technical drafting error in COBS 12.2.21R(1)(f), introduced when the MiFID Organisational Regulation was transferred to the Handbook. The current wording inadvertently changed the meaning and may be interpreted as more restrictive on firms than intended. The FCA proposes to revert to the original drafting.

Although the FCA is not consulting on further changes at this stage, it seeks feedback on the following discussion questions on the remaining aspects of the 2018 rules in order to explore further opportunities for reform:

The proposals represent a concerted effort by the FCA to address consistent market feedback on the 2018 reforms and form part of the UK regulator’s broader strategy to support growth and improve the competitiveness of the UK as a listing venue. Responses to the consultation are requested by 29 May 2026, following which the FCA will consider the feedback and publish a policy statement subject to finalising the rules.

Authored by Daniel Simons and Danette Antao.

.jpg?sc_lang=en)