.jpg)

EU-UK Spotlight: Renewables, trade, and the global supply chain

Search

Search

Search

Search

ATAD 2 amends the European Directive 2016/1164 of 12 July 2016 laying down rules against tax avoidance practices in the EU that directly affect the functioning of the internal market (so-called "ATAD Directive"), which has been implemented in Luxembourg by the law of 21 December 2018 ("ATAD Law"), commented in our blog article dated 18 December 2018.

Hybrid mismatches arrangements exploit differences in the tax treatment of an entity or instrument under the laws of two or more jurisdictions to achieve either a double deduction or a deduction without inclusion. Although the ATAD Directive and the ATAD Law already contain provisions to neutralize hybrid mismatches effects ("Hybrid Mismatches Rules"), the latter only apply within the EU and cover a limited number of transactions. The aim of ATAD 2 is to extent the scope of the Hybrid Mismatches Rules to a broader range of transactions and also to apply to transactions with non-EU countries.

In essence, the Hybrid Mismatches Rules set out in the ATAD 2 Law include four main categories2 :

These Hybrid Mismatches Rules contain further specific provisions related to imported hybrid mismatches, tax residency mismatches, hybrid transfers and reverse hybrid mismatches.

Most of the measures of the ATAD 2 Law are applicable as from 1 January 2020, whilst the remaining ones will be applicable as of the taxation year 2022.

Check out our article to get more detailed information regarding the key topics of the ATAD 2 Law.

According to the ATAD 2 Law, a hybrid mismatch may only exist if differences occur between associated enterprises, between the taxpayer and an associated enterprise, between the head office and the permanent establishment, between two permanent establishments or more or in the context of a structured arrangement. In this context, the ATAD 2 Law replaces article 168ter of the LITL, which contained already limited provisions to neutralize the effects of hybrid mismatches as implemented in Luxembourg by the ATAD Law. The new 2020 version of article 168ter LITL reshapes the concept of associated enterprises and provides a definition regarding the concept of structured arrangement. In addition, it introduces a new concept of "acting together".

In its 2019 version, article 168ter LITL already referred to the concept - although more restrained - of associated enterprise. However, the latter was not defined in the article 168ter LITL itself but only by means of cross-references to article 164ter LITL on controlled foreign companies.

The ATAD 2 Law now directly introduces in the body of the new article 168ter LITL a comprehensive definition of an associated enterprise, being:

In addition, if an individual or entity holds directly or indirectly a participation of at least 50% in terms of voting rights or capital ownership in both the taxpayer and one or more entities, all these entities, including the taxpayer, will be considered as associated enterprises.

In case of hybrid mismatches involving a financial instrument, the threshold of 50% is replaced by a threshold of 25%.

To avoid that the threshold of 50% in relation to associated enterprises is circumvented by notably splitting the holding of the participation into several persons or entities, the ATAD 2 Law provides that an individual or entity who is acting together with another individual or entity in respect of the voting rights or capital ownership of an entity shall be treated as holding a participation in all of the voting rights or capital ownership of that entity that are held by the other individual or entity. As such, the percentages of these persons involved are aggregated for the purposes of the 50%threshold.

However, the ATAD 2 Law provides a rebuttable presumption in relation to investment funds. Indeed, an individual or an entity, which holds directly or indirectly, less than 10% of the shares or interests in an investment fund and is entitled to receive less than 10% of the profits thereof, is deemed not to act together with another person or entity which also holds shares or interests in such investment fund.

Article 168ter LITL, in its 2019 version, referred to the concept of structured arrangement but did not give a definition in respect thereof. Article 168ter LITL, in its new version as implemented by the ATAD 2 Law, introduces a definition of this concept, being an arrangement involving a hybrid mismatch where the mismatch outcome is priced into the terms of the arrangement or an arrangement that has been designed to produce a hybrid mismatch outcome, unless the taxpayer or an associated enterprise could not reasonably have been expected to be aware of the hybrid mismatch and did not share in the value of the tax benefit resulting from the hybrid mismatch.

The ATAD 2 Law addresses in fact eleven categories of hybrid mismatches:

These different kinds of hybrid mismatches are detailed below.

There will be an hybrid mismatch if the payment under a financial instrument gives rise to a deduction without inclusion outcome and;

(i) the mismatch outcome is attributable to differences in the characterization of the instrument or the payment made under it; and

(ii) such payment is not included within a "reasonable period of time".

Example:

.jpg)

A "reasonable period of time" is characterized if:

(i) the payment is included by the jurisdiction of the payee in a tax period that starts within 12 months of the end of the payer's tax period; or

(ii) it is reasonable to expect that the payment will be included by the jurisdiction of the payee in a future tax period and the terms of payment are those that would be expected to be agreed between independent enterprises.

The ATAD 2 Law excludes from the scope of this hybrid mismatch certain financial instruments or situations.

Firstly, a payment representing the underlying return on a transferred financial instrument shall not give rise to a hybrid mismatch where the payment is made by a financial trader under a hybrid transfer, which is entered into by the financial trader in the ordinary course of business, and not as part of a structured arrangement, provided the payer jurisdiction requires the financial trader to include as income all amounts received in relation to the transferred financial instrument.

Secondly, Luxembourg has implemented the option given by ATAD 2 to exclude from its scope, until 31 December 2022, payments to an associated enterprise under a financial instrument with conversion, bail-in or write down features, provided among others that such instrument has been issued for the sole purpose of satisfying loss absorbing capacity requirements applicable to the banking sector and not as part of a structured arrangement.

Finally, based on the preliminary considerations of ATAD 23 and in line with the opinion of the Luxembourg State Council (Conseil d’Etat)4, two other situations should be excluded from the scope of hybrid mismatches:

(i) the differences in tax outcomes that are solely attributable to differences in the value ascribed to a payment, including through the application of transfer pricing, will not fall within the scope of a hybrid mismatch; and

(ii) where the tax relief granted in the payee jurisdiction is solely due to the tax status of the payee or the fact that the instrument is held subject to the terms of a special regime.

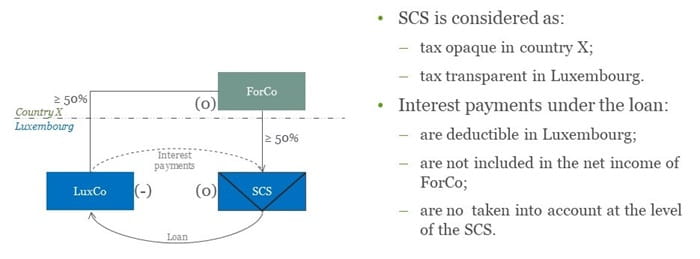

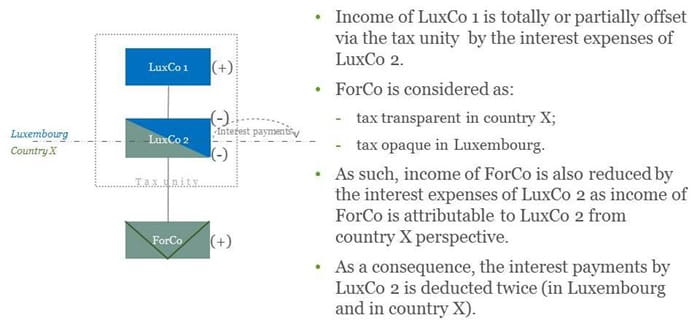

There will be an hybrid mismatch if a payment to an hybrid entity gives rise to a deduction without inclusion and that mismatch outcome is the result of differences in the allocation of payments made to the hybrid entity under the laws of the jurisdiction where the hybrid entity is established or registered and the jurisdiction of any individual or entity with a participation in that hybrid entity.

An hybrid entity is defined as any entity or arrangement that is regarded as a taxable entity under the laws of one jurisdiction and whose income or expenditure is treated as income or expenditure of one or more other individuals or entities under the laws of another jurisdiction.

Example:

This hybrid mismatch should only apply where the mismatch outcome is a result of differences in the rules governing the allocation of payments under the laws of the two jurisdictions, and a payment should not give rise to a hybrid mismatch that would have arisen in any event due to the tax exempt status of the payee under the laws of any payee jurisdiction.5

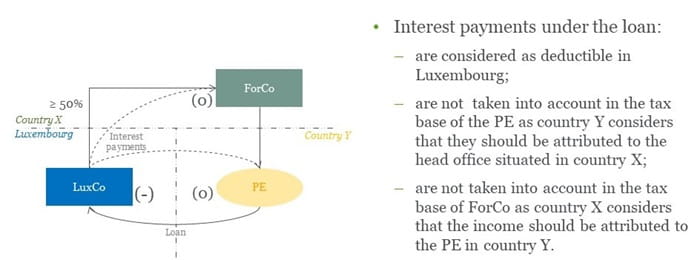

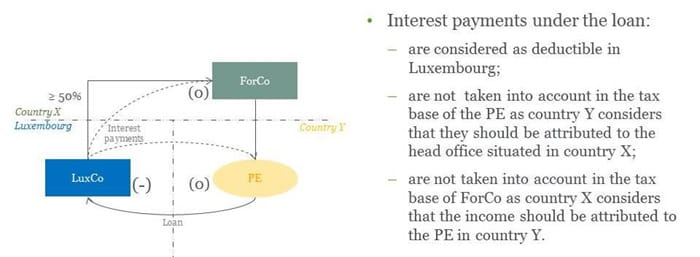

There will be a hybrid mismatch if a payment to an entity with one or more PEs gives rise to a deduction without inclusion and that mismatch outcome is the result of differences in the allocation of payments between the head office and permanent establishment or between two or more permanent establishments of the same entity under the laws of the jurisdictions where the entity operates.

Example:

This hybrid mismatch should only apply where the mismatch outcome is a result of differences in the rules governing the allocation of payments under the laws of the two jurisdictions, and a payment should not give rise to a hybrid mismatch that would have arisen in any event due to the tax exempt status of the payee under the laws of any payee jurisdiction6.

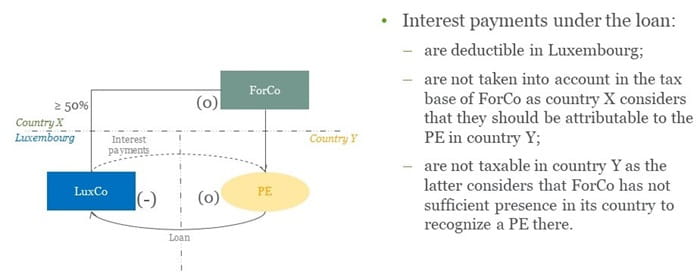

There will be a hybrid mismatch if a payment gives rise to a deduction without inclusion and that mismatch outcome is the result of a payment to a disregarded permanent establishment.

Example:

This hybrid mismatch rule should not apply, however, where the mismatch would have arisen in any event due to the tax exempt status of the payee under the laws of any payee jurisdiction7.

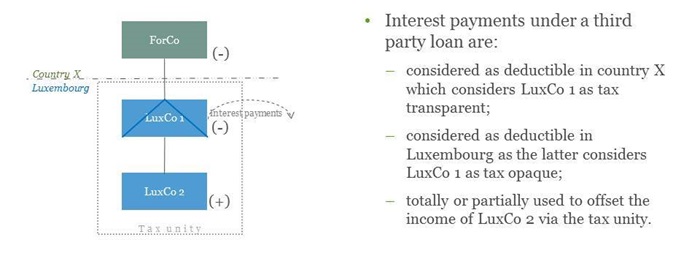

There will be a hybrid mismatch if a payment by a hybrid entity gives rise to a deduction without inclusion and that mismatch is the result of the fact that the payment is disregarded under the laws of the payee jurisdiction.

Example:

This hybrid mismatch rule should not apply, however, where the payee is exempt from tax under the laws of the payee jurisdiction8.

Finally, no mismatch outcome should arise under this hybrid mismatch to the extent that the payer jurisdiction allows the deduction in respect of the payment to be set off against an amount that is dual-inclusion income.

There will be a hybrid mismatch if a deemed payment between the head office and its PE or between two or more permanent establishments gives rise to a deduction without inclusion and that mismatch is the result of the fact that the payment is disregarded under the laws of the payee jurisdiction.

Example:

This hybrid mismatch rule should not apply, however, where the payee is exempt from tax under the laws of the payee jurisdiction .

Finally, no mismatch outcome should arise under this hybrid mismatch to the extent that the payer jurisdiction allows the deduction in respect of the deemed payment to be set off against an amount that is dual-inclusion income.

There will be a hybrid mismatch if a double deduction occurs.

A double deduction is defined by the ATAD 2 Law as a deduction of the same payment, expenses or losses in the jurisdiction in which the payment has its source, the expenses are incurred or the losses are suffered (payer jurisdiction) and in another jurisdiction (investor jurisdiction). In the case of a payment by a hybrid entity or permanent establishment the payer jurisdiction is the jurisdiction where the hybrid entity or permanent establishment is established or situated.

Finally, no mismatch outcome should arise under this hybrid mismatch to the extent that the payer jurisdiction allows the deduction in respect of the payment to be set off against an amount that is dual-inclusion income.

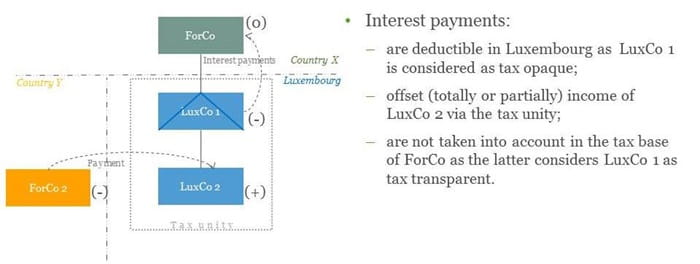

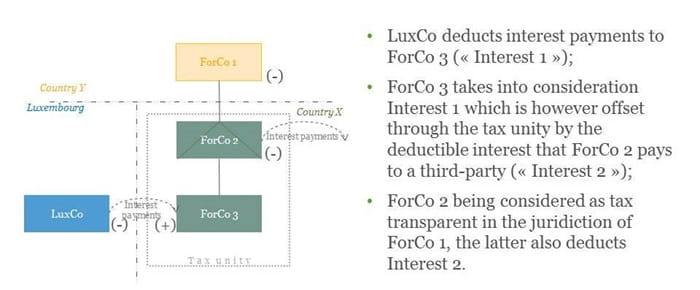

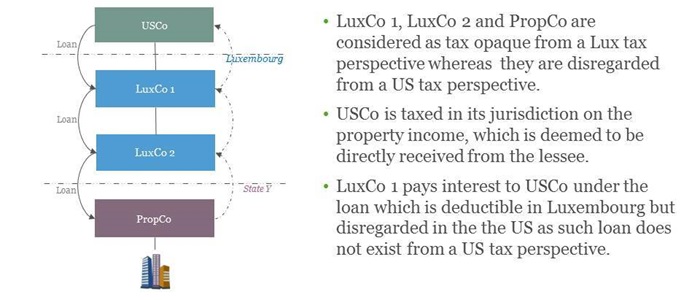

There will be an imported hybrid mismatch if through the use of a non-hybrid instrument, the effect of a hybrid mismatch between parties in third countries will be shifted to Luxembourg. For instance, a deductible payment in Luxembourg can be used to fund expenditure involving a hybrid mismatch.

Example 1 (deduction without inclusion):

Example 2 (double deduction):

A dual (or plural) resident mismatch could lead to a double (or plural) deduction if a payment made by a dual (or plural) resident taxpayer is deducted under the laws of both (more) jurisdictions where the taxpayer is resident.

Example (dual tax residency mismatch):

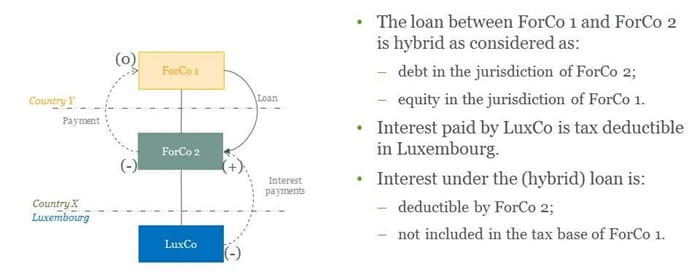

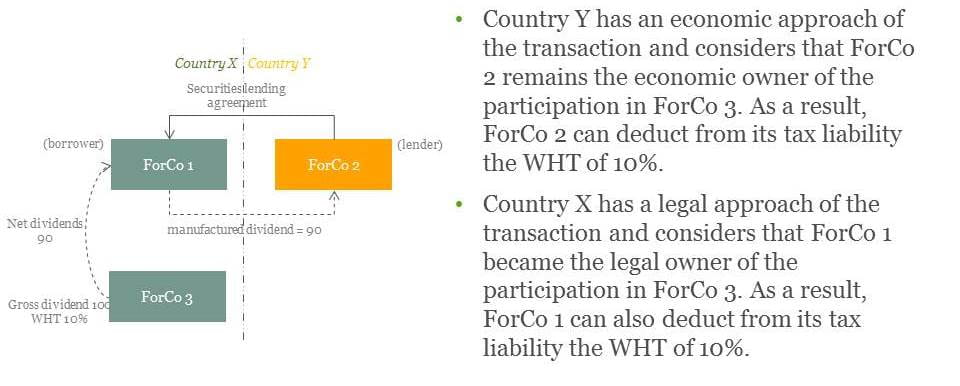

There will be a hybrid transfer in presence of a difference in tax treatment if, as a result of an arrangement to transfer a financial instrument, the underlying return on that instrument was treated as derived by more than one of the parties to the arrangement.

A hybrid transfer is defined by the ATAD 2 Law as any arrangement allowing the transfer of a financial instrument where the underlying return on the transferred financial instrument is treated for tax purposes as derived simultaneously by more than one of the parties to that arrangement.

A hybrid transfer may generally occur when the laws of two jurisdictions take opposing views on who is the owner of the underlying return on the transferred asset, especially when a party established in one jurisdiction has a legal approach of the transaction whereas the counterparty established in another jurisdiction has an economic approach, such difference leading to double benefits, notably in terms of tax credits.

Example (securities lending):

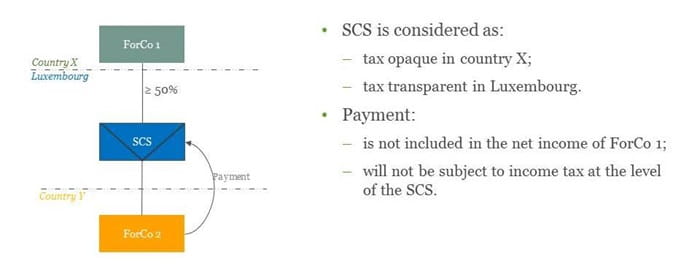

Article 168quater LITL will, however, not be applicable to collective investment vehicles ("Exempt CIV"). For the purposes of article 168quater LITL, an Exempt CIV is defined as an investment fund or vehicle that is widely held, holds a diversified portfolio of securities and is subject to investor-protection regulation. According to the commentaries of the ATAD 2 Bill9, the definition of Exempt CIV should include the following:

In line with ATAD 2, the ATAD 2 Law provides for different methods to tackle the negative hybrid mismatch effects, depending on either their outcomes or the hybrid mismatch itself.

If a hybrid mismatch results in a double deduction:

Nevertheless, any such payments, expenses or losses will remain tax deductible against a dual-inclusion income occurred during the current tax period. Payments, expenses or losses that couldn't be used for tax purposes during the current tax period may be carried forward to a subsequent tax period and remain tax deductible therein against dual-inclusion income occurred during such subsequent tax period.

If a hybrid mismatch results in a deduction without inclusion:

The secondary rule will, however, not be applicable to certain hybrid mismatches.

In case of imported hybrid mismatches, payments which have financed, directly or indirectly, deductible expenses giving rise to a double deduction or a deduction without inclusion between third countries under a hybrid mismatch are disallowed at the level of Luxembourg payer, unless an adjustment has been made in one of the jurisdictions involved in the hybrid mismatch.

To the extent that a hybrid mismatch involves disregarded permanent establishment income which is tax exempt in the hands of a Luxembourg taxpayer according to a double tax treaty between Luxembourg and a EU Member State, the Luxembourg taxpayer will have to include, in its net income, the income that would otherwise be attributed to the disregarded permanent establishment.

To the extent that a deduction for payments, expenses or losses of a Luxembourg taxpayer who is resident for tax purposes in two or more jurisdictions is deductible from the tax base in both or more jurisdictions, the Luxembourg taxpayer will have to deny the deduction for such payments, expenses or losses except if they relate to dual-inclusion income.

Such payments, expenses or losses will remain tax deductible in Luxembourg if the other jurisdiction is a EU Member State with which Luxembourg has concluded a double taxation treaty under which the taxpayer is deemed to be a Luxembourg resident.

To the extent that a hybrid transfer is designed to produce a relief for tax withheld at source on a payment derived from a transferred financial instrument to more than one of the parties involved, the Luxembourg taxpayer will have to limit the benefit of such relief in proportion to the net taxable income regarding such payment. In addition, the portion of foreign withholding tax which has not been deducted against the net taxable income will not be deductible from the tax base of the Luxembourg taxpayer.

According to article 168quater of the LITL, once applicable, Luxembourg tax transparent entities, as well as arrangements incorporated or established in Luxembourg, whose net income is considered as the net income of one or more other individuals or entities, will be considered as resident taxpayers and taxed on their income to the extent that this income is not otherwise taxed under the ATAD 2 Law or the laws of any other jurisdiction, provided that one or more associated non-resident entities holding in aggregate a direct or indirect interest in 50% or more of the voting rights, capital interests or rights to a share of profit in such Luxembourg entities or arrangements are located in a jurisdiction or jurisdictions that regard the these Luxembourg entities or arrangements as a taxable person.

In line with the opinion of the Luxembourg State Council (Conseil d’Etat)10, the ATAD 2 Bill has been amended to specify that article 168quater LITL only applies prorate to the net income that may fall under its provision, and does thus not directly render the Luxembourg entity or arrangement as an entirely Luxembourg taxable person.

Whilst implementing the provisions of ATAD 2 rather literally into Luxembourg law, the ATAD 2 Law, includes certain points that would need confirmation, clarification or written guidance. Some of these points are highlighted below and, in the meantime, our team is happy to assist with question on any of them.

Authored by Gérard Neiens, Jean-Philippe Monmousseau, Pierre-Luc Wolff, and Grâce Mfuakiadi

Hogan Lovells (Luxembourg) LLP is registered with the Luxembourg bar.

.jpg?sc_lang=en)